Global forest industry results in the Q4/2016 are shown below.

Global Timber Markets

With a few exceptions, sawlog prices were lower throughout the world in the 4Q/16 than they were in the previous quarter. The Global Sawlog Price Index (GSPI) fell 1.2% to US$69.82/m3 in the 4Q/16. The current GSPI is up 1.4% from a year ago but over 13% lower than in the same quarter two years ago.

Sawlog prices in Europe have been trending downward the past three years from their record high levels in 2014. The European Sawlog Price Index (ESPI-€) was €83.16/m3 in the 4Q/16, 8.2% below its peak in the 1Q/14. Sawlog prices in Sweden, Finland and Norway are currently at their lowest levels in over ten years in their local currencies despite healthy lumber markets for the sawmills in the region.

Global Pulpwood Prices

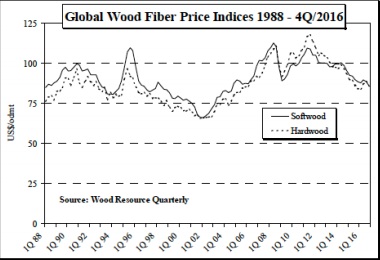

Both wood fiber price indices fell in the 4Q/16, with the SFPI declining 3.2% q-oq to $85.65/odmt, and the HFPI falling 2.6% to $86.16/odmt.

Softwood fiber prices were down in most of Europe and North America, while they increased in Latin America, Russia, Oceania and Asia in the 4Q/16. The biggest declines occurred in Canada, Sweden and Germany, where prices in US dollar terms were lower because of reduced prices in the local currencies and a stronger US dollar.

Hardwood fiber prices followed the same pattern as that of softwood prices, with generally lower prices in Europe and North America q-o-q, while prices were slightly higher in Latin America and Oceania. In Russia, prices were up over 11% from the 3Q/16.

Global Pulp Markets

During the first 11 months of 2016, global market pulp production was up 3.4% as compared to the same period in 2015. The rise in production in 2016 is a continuation of an upward trend that started in 2011.

Softwood pulp prices have been quite stable throughout 2016 and indications early in 2017 are that pulp producers in North America and Europe are pushing for price increases during the first quarter, as markets are strengthening.

Prices of hardwood pulp (BHKP) fell during much of 2016. In Europe, prices in the end of 2016 were at their lowest levels in five years.

Global Lumber Markets

Global softwood lumber trade increased 12 percent year-over-year in 2016 to reach a new record-high of 121 million m3, according to estimates by WRI. Since the global financial reception in 2009, there has been a steady climb in international trade of lumber with shipments the past seven years having increased as much as 66 percent.

Lumber exports from British Columbia are on pace to reach their highest levels since 2006 this year.

Lumber prices in the US trended upward during most of 2016 but plateaued late in the year and in early 2017. Current prices are close to the highest levels in almost two years.

Although prices increased in both Finland and Sweden during the spring and summer of 2016, this upward trend was short-lived and prices fell during the fall, and in the 4Q/16, were back down to about the same level as in the 4Q/15.

Despite relatively pessimistic forecasts for wood demand early in 2016, China’s need for imported wood picked up during the summer and fall with import volumes in the 4Q/16 being up about 20% as compared to the 4Q/15.

Global Biomass Markets

US pellet exports increased to 1.16 million ton in the 3Q/16, with all the volume headed to Europe. US pellet exports to Asia have dried up with no significant volumes having been recorded in the past five quarters.

Prices for residential pellets in Germany have increased for two consecutive quarters and are currently at their highest level in two years