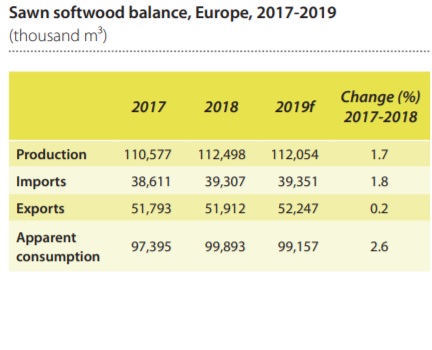

The European market showed steady growth in 2018, with consumption rising to 99.9 million m3; it is expected to ease in 2019, however, the major consuming countries in Europe had mixed performances in 2018. Consumption increased by 0.8% in Germany, the largest sawn softwood market in Europe, to a record 19.5 million m3 .

The UK is the second-largest consuming country in Europe but, after two years of remarkable growth, consumption there dropped by 7.6% in 2018, to 9.8 million m3. Consumption was flat in France, at 8.2 million m3 .

The Baltic states are importing increasing quantities of sawn softwood from other European countries and the Russian Federation. Estonia has the highest sawn softwood consumption per capita in Europe, and Latvia is number three behind Austria.

Production and capacity change

Production and capacity change

Sawn softwood production grew by 1.7% in Europe in 2018, to 112.5 million m3. The increase was driven more by European demand than by overseas exports, with demand declining in the key markets of China and Japan.

Production increases in central Europe were clearly above European averages, due partly to timber salvage programmes there to harvest trees damaged by storms or beetles. Output from the Nordic mills was more moderate, with production volume steady in Sweden in 2018, at 18.3 million m3, and Finnish production up by 0.8%, to 11.8 million m3. The biggest absolute gains in Europe in 2018 were in Germany (+2.5%) and Austria (+5.6%), both up by more than 500,000 m3, and there was also an increase of more than 300,000 m3 (+5.5%) in Turkey.

In addition to the large volumes of salvage timber available (beetle attacked, windthrow, etc.), the growth in sawn softwood production in the European subregion in 2018 was due to improved capacity utilization at existing mills and the debottlenecking of production equipment. There were no major greenfield investments or closures in the sawmill industry in Europe in 2018.

Prices

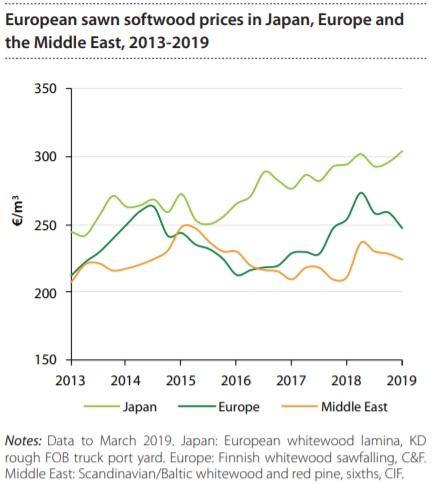

Prices increased for European sawn softwood in the first half of 2018 in Japan, Europe and the Middle  East, but the trend changed in the second half of the year.

East, but the trend changed in the second half of the year.

The price for Finnish whitewood (cost & freight, C&F) in Europe increased to the middle of the year but declined sharply in the fourth quarter; nevertheless, it was 12% higher (in euros per m3 ) in 2018 than in 2017. Prices increased in the Middle East for European sawn softwood but still lagged behind those in Europe. The price for Scandinavian/ Baltic sawnwood (cost, freight & insurance; CIF) was up by 6% (in euros per m3) compared with 2017, and the year-on-year price in the first quarter of 2019 was also 6% higher.

The price trend in Japan for European sawn softwood was relatively stable in the local currency (yen) in 2018, although there was a moderate decline in the second quarter; the price was steady thereafter to the first quarter of 2019. Overall, there was a decline of only 1% in 2018 (free-on-board – FOB – truck Japanese port) in euro terms as the yen strengthened.

On the other hand, the price was up by 3%, year-on-year, in the first quarter of 2019.

Trade

Imports

European imports of sawn softwood increased by 1.8% in 2018, to 39.3 million m3 . The clear majority of imports are intrasubregional. Extra-subregional imports originate mainly in Belarus, the Russian Federation and Ukraine. Imports increased from Belarus (by 1.0 million m3 ) and Ukraine (0.6 million m3 ). Europe imported a total of about 4.8 million m3 from these two countries in 2018. Imports also increased from the Russian Federation (by 8%), to 3.8 million m3 .

European imports of sawn softwood increased by 1.8% in 2018, to 39.3 million m3 . The clear majority of imports are intrasubregional. Extra-subregional imports originate mainly in Belarus, the Russian Federation and Ukraine. Imports increased from Belarus (by 1.0 million m3 ) and Ukraine (0.6 million m3 ). Europe imported a total of about 4.8 million m3 from these two countries in 2018. Imports also increased from the Russian Federation (by 8%), to 3.8 million m3 .

The UK, Germany and Italy are the largest importers of sawn softwood in the subregion, accounting for 40% of the total volume. Imports to the UK and Italy declined by 11% and 4.6%, respectively, in 2018 but increased by 6.0% in Germany.

Exports

The volume of European sawn softwood exports was steady (+0.2%) in 2018, at 51.9 million m3. There was an increase in intraregional exports within Europe, but demand declined in the key overseas markets of China and Japan. Of the major exporters, volumes increased from Austria and Germany but fell slightly from Finland and Sweden. Central European suppliers had a clear advantage over Nordic producers in lower log prices due to salvaging programmes for timber damaged by storms and beetles.

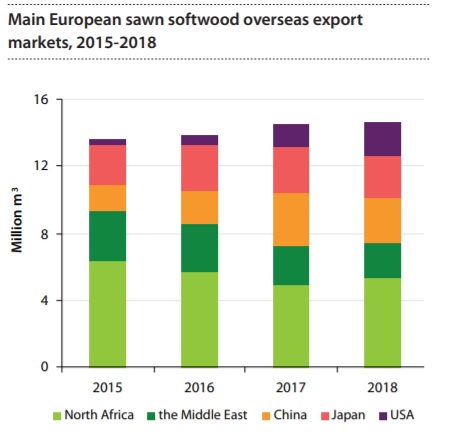

European overseas exports of sawn softwood show strong regional variation and declined slightly (0.3%) overall in 2018. Combined exports to the MENA region (Middle East and North Africa) increased by 3.6% in 2018 after a sharp drop in 2017. Exports to Egypt (the largest market in the region) continued to decline, but positive developments in North Africa, including a sharp increase – a near-doubling – in exports to Algeria, compensated for the volumes lost to Egypt and the Middle East. Exports of European sawn softwood to Egypt picked up in the first quarter of 2019 and leapt overall by 20% in North Africa.

The rapid growth in European exports to China came to an end in 2018. High stock levels combined with declining prices and increased exports from the Russian Federation resulted in a 25% drop in European exports to China compared with 2017, to 2.5 million m3. Finland and Sweden – the main European exporters – took the hardest hit. This declining trend continued into the first quarter of 2019, with European exporters losing market share to the Russian Federation, despite increased imports to China.

There was also a substantial drop (-9.4%) in European exports to Japan, to 2.5 million m3, with only Austria increasing its trade. Japan’s overall import volume declined by 6% in 2018, and Europe therefore lost market share to Chile, the Russian Federation and the US. Exports from Europe to Japan were also down (by 5%) in the first quarter of 2019 due to tight market conditions.

European exports to the US continued to expand rapidly in 2018 (up by 54% to 2.0 million m3). Half these exports were from Germany, followed by Sweden, Austria and Romania.