Global Wood Markets Info spoke with Erik Eliasson, Sales Director at Norra Timber, about the current state of the Swedish sawmill industry, log supply, export markets and the outlook for the rest of 2026.

Erik has served as Sales Director at Norra Timber since 2010 and has a long background in the wood industry. Raised in a sawmill entrepreneur family, he developed an early understanding of the sector before studying business economics and later holding senior roles in sawmill trade, sales management and company leadership.

Norra Timber is one of northern Sweden’s major forest industry companies. The cooperative is owned by 27,000 private forest owners, managing around 2.2 million hectares of forest land. The company employs 620 people and operates three sawmills with total capacity of 900,000 m³, two planing mills producing 250,000 m³ annually, and a pole factory manufacturing 75,000 poles per year.

Norra Timber also owns 30% of the Husum pulp mill, which has annual capacity of 750,000 tonnes, and has annual turnover of approximately €0.5 billion.

Erik is also Chairman of the Market Committee at the Swedish Forest Industries Federation and is frequently invited as a speaker and industry analyst on global wood markets, price developments, demand trends and strategic shifts in the sawmill sector.

GWMI: How would you describe the current state of the Swedish sawmill industry in 2026, and what are the main challenges and opportunities for producers?

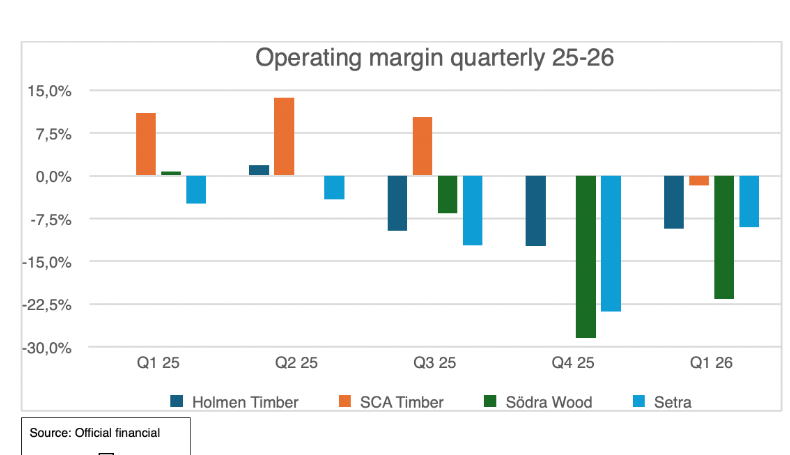

Erik Eliasson: Swedish sawmills face ongoing difficulties, with tight log supply and still too high log costs—especially concerning the disparity between spruce and pine availability. Pine now accounted for as much as 44 % of total production in 2025. While both sawlog and pulp log prices are beginning to drop, many sawmill companies continue to report big losses, particularly in the south (see attached graph). Industry grid prices remain elevated, prompting companies to cut back on production. Since about half of Sweden's forests are privately owned—and owners expect high payments for harvesting—many are unwilling to sell unless prices match their expectations, leading to reduced harvesting levels. One exception is the storm-driven harvesting underway in central Sweden, temporarily adding about 5 million m³ of sawlogs. From January to March, overall production dropped by 8%, though central Sweden saw a 5% rise due to storm fellings.

Currency fluctuations also impact the market. In 2025, the Swedish krona strengthened by almost 18% against the US dollar, but it has since weakened due to the Iran conflict, affecting the entire forest sector, including paper and pulp. Market uncertainty, heightened by geopolitical tensions and new US trade policies, has damaged buyer confidence and increased freight costs. Although there was domestical previously a positive outlook for 2026—with higher real incomes, lower taxes, low inflation and reduced interest rates in Sweden—confidence has largely diminished.

The most significant opportunities are including pine in the construction assortment. Swedish wood has now opened up planned pine as an official construction product alone or mixed with spruce. Many mills therefore substitute spruce with pine in their production. Many mills focus on maximizing yield with high technology investments. Such as CT scanning installations and better log grading.

GWMI: How have European lumber exports evolved over the past year, especially regarding the Middle East, North Africa, and Asia? Have recent geopolitical issues and freight disruptions affected trade or customer behavior?

Erik Eliasson: Exports to the United States have declined significantly, particularly from Central Europe, registering a decrease of 33% in Q1 compared to 25% previously. This downturn is attributed to factors such as constrained low-quality production, U.S. trade policies, and pricing issues. Asian markets, including China and Japan, are also experiencing reduced demand; notably, China's decline is pronounced due to a weakening construction sector, while Russia continues to hold a dominant position in the Chinese lumber market. The Japanese market has remained relatively stable, and it is anticipated that Scandinavian producers will maintain their leading market share, accounting for 35-40% of Japan's imports.

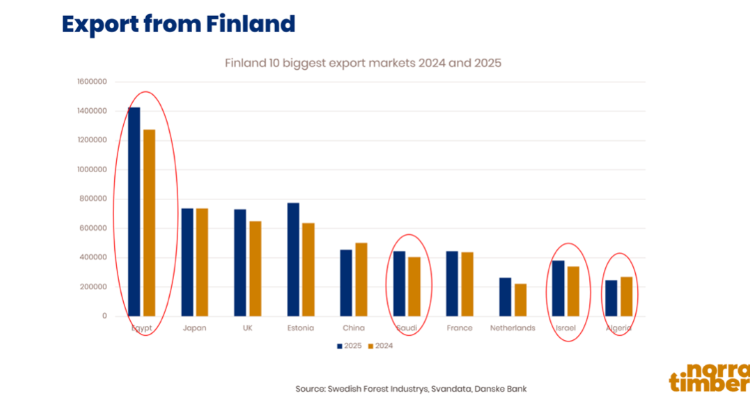

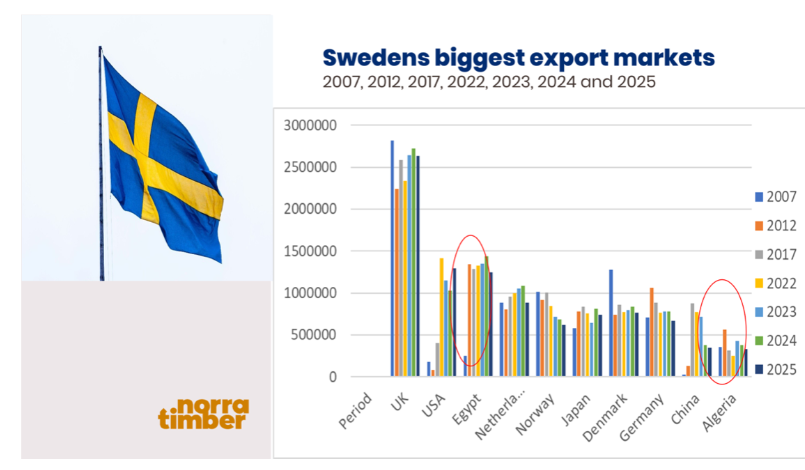

Conversely, Scandinavian pine exports to the MENA region are increasing, with rising demand observed in countries such as Morocco, Egypt, and Algeria. Last year, Egypt emerged as Finland’s largest and Sweden’s second-largest export destination. As pine production grows, MENA markets are becoming increasingly important. Freight costs have risen sharply—by as much as 20% for break bulk vessels—due to the conflict in the Strait of Hormuz, leading to reduced shipment availability. Additionally, the lack of return freight from the MENA region has created logistical challenges for shipping companies. For Swedish exporters, deliveries transiting through the Strait of Hormuz total approximately 400,000 m³, thus the direct impact remains limited. However, increased freight costs and reduced shipping options, coupled with greater uncertainty, are presenting additional challenges.

GWMI: What is the present situation regarding sawlog supply and log prices in Sweden? Are elevated raw material costs still a primary concern for sawmills, particularly in northern regions?

Erik Eliasson: Sawlog and pulpwood prices in Sweden are declining rapidly in central and southern regions after previously reaching record levels. Prices in southern Sweden can’t drop to much because otherwise the market becomes too competitive for German importers. In central Sweden, a recent storm has temporarily allowed sawmills to acquire logs at reduced price levels, with the storm expected to deliver approximately five million cubic meters of sawlogs over the next two quarters—about 13% of Sweden’s annual log consumption. Despite these price decreases, many forest owners are reluctant to harvest, anticipating higher rates in the future, which may result in supply shortages. In northern Sweden, price fluctuations are a bit less pronounced, limiting potential reductions. The region instead faces challenges related to indigenous rights, conservation measures, and species protection, alongside continued downward pressure on wood chip and pulpwood prices. Therefore, although the situation is not ideal, other factors besides raw material costs contribute to ongoing concerns in the north.

GWMI: Can you summarize recent price trends for Swedish lumber products? Are there particular export markets or product segments with stronger demand?

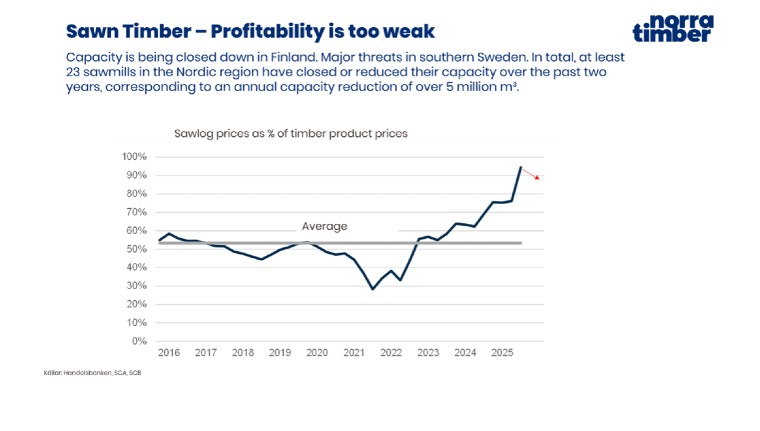

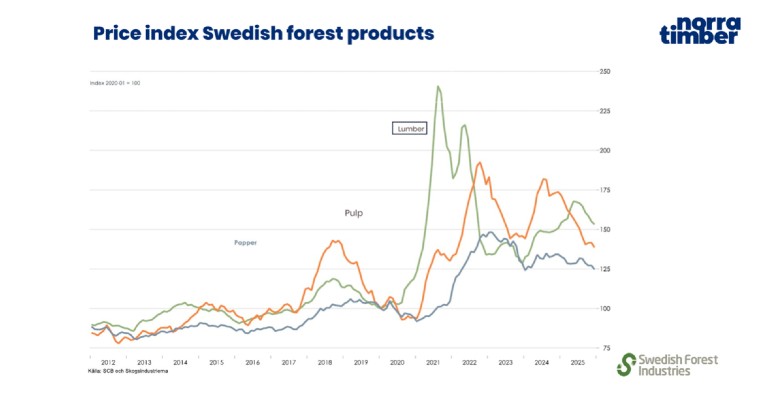

Erik Eliasson: Prices rose during the second quarter, especially for spruce assortments, while pine remains more challenging but shows slight gains. Central Europe has increased imports of glulam and cross-laminated timber (CLT) as domestic production decreases. Demand for pine is growing in MENA countries like Morocco, Algeria, Jordan, and Egypt. In those markets we now see an upturn in prices beyond compensation for higher freight. Generally, from a long term 10-year perspective lumber prices are high today. In fact, except for the Covid era, it hasn’t been higher prices. See graph below.

GWMI: What are your expectations for the rest of 2026 regarding lumber demand, exports, sawlog prices, and the general market outlook in Europe?

Erik Eliasson: Scandinavian production is expected to continue to decline in autumn due to weak log supply, leading to reduced output and exports. If the Iran conflict resolves, buyer confidence could return and boost market activity. Companies with reliable log sources will be in a stronger position. My assumption is that the mills with stable log supply will be winners under the second half of the year. Mainly by declining production, which is caused by lack of saw logs to competitive prices among many of the mills. Those mills will struggle to get enough saw logs, and the risk is that they won’t get enough logs.